Q3 2025 Market Insights

The branded residential market is playing the long game in Q3 2025, with the sector’s appetite for further expansion remaining strong as it heads into the final quarter of the year. As of Q3 2025, the sector’s pipeline stood at 1,037 projects versus 795 completed developments, with the pipeline-to-existing inventory gap widening to more than 240 projects. This points toward sustained openings from 2026 through to 2034, while the year-on-year context highlights real-time growth, with completed schemes rising from 755 in Q3 2024.

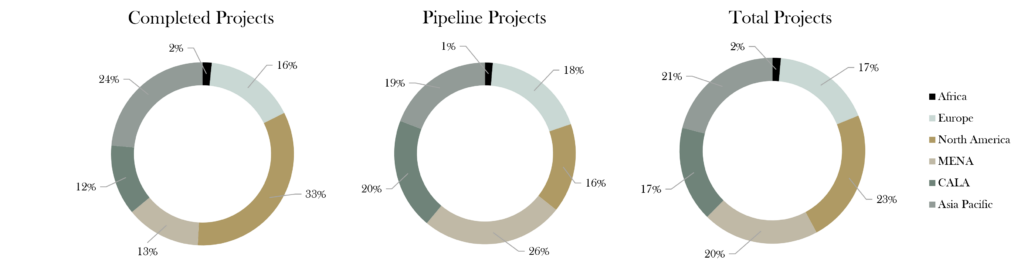

This quarter’s most notable region is MENA – recording the highest number of projects converting to completed status while also contributing the largest share of new additions to the Q3 2025 pipeline. At the city-level, we now see Abu Dhabi overtake Cairo in the region’s top 3 city ranking, with Abu Dhabi’s branded residential market expected to grow by 5 times by 2030! On a global top city ranking level, we now see São Paulo overtake New York City (completed and pipeline combined) and claim the global third spot. In APAC, Thailand regains the first spot, pushing Vietnam to second place. Comparing Q3 2025 to Q3 2024, MENA is now the main driver of pipeline growth. In contrast, Q3 2024 growth was largely driven by Europe, mainly Georgia and Spain. North America (a leader when it comes to the global completed branded residential projects with a 33% share) contributed only 6.5% to this quarter’s growth. This proves a constant regional shift with all regions fighting for a share, and, perhaps, a strategic shift toward more emerging markets within individual regions with higher growth trajectory.

Looking at the pipeline of all projects on a global level, and not just the Q3 2025 growth, the end of Q3 2025 shows MENA with a share of 26%, followed by CALA (20%) APAC (19%), Europe (18%), and North America (16%). It seems like different regions now show increased appetite for the branded residences market, slowly balancing out the global market overview / share.

Regarding development context, the cities are winning, with the quarter’s added pipeline revealing a city-driven growth, as half of all new projects are targeting Urban, and around 14% are targeting Urban-Resort locations. Year-on-year context shows 45% of all completed and pipeline developments in Urban settings as of Q3 2024, but also in Q3 2025 – showing that this quarter’s growth is mostly a quarterly and temporary shift, rather than a new trend towards more Urban locations.

In terms of development type, Standalone developments contribute 52% of the Q3 2025 pipeline growth, further increasing the Standalone share in the global branded residential market. On the branding front, while hotels still dominate the space – with Marriott and Accor leading the ranks – fashion and other non-hospitality brands are making a surprisingly strong entrance in strategic markets.

This quarter’s Market Spotlight section focuses on amenities and facilities, as well as the expected trends for these sector-defining features across both hotel, and non-hotel branded developments.