Q4 2025 Market Insights

The branded residential sector closes out 2025 on a confident note, adding 100 projects in Q4 – 92 in the pipeline and 8 already completed, bringing the global total to 1,907 developments by year-end. Of those, 830 are completed and 1,077 remain in the pipeline, with the pipeline-to-completed gap representing approximately 13% of total global supply this quarter. The quarter’s completed and pipeline additions represent approximately 14,310 new residential units, and the market’s direction remains: the sector is not slowing down, it is loading up.

Hospitality brands lead, lifestyle follows; Hotel brands account for 90% of Q4 additions, with Marriott and Accor leading all parent brands, followed by Wyndham, Hilton, Radisson, and Hyatt. The non-hotel 10% is headlined by Fashion brands at 40%, with Design and F&B each at 20% and Nobu emerging as the standout non-hotel brand of the quarter. Luxury holds firm at 65% of additions, with Upper Upscale at 18%, confirming that, at least for the now, this sector continues to trade overwhelmingly at the top end of the market.

Resorts reclaims ground, Standalone continues to expand; After Q3’s urban-leaning growth, Q4 tilts toward resort settings at 41%, with Urban at 39% and Urban-Resort at 20%. This is a quarterly shift rather than a structural one, as the longer-term urban trend remains intact across the total completed and pipeline market. Hotel Co-Located projects lead on development type at 40%, marginally ahead of Standalone (36%) and Integrated (24%). Despite this, Standalone’s cumulative global share continues to grow, pointing to sustained developer and market appetite for independent, brand-led residential products.

A more balanced regional picture – with MENA still setting the pace; Regionally, MENA leads Q4 growth at 27.8%, followed by APAC at 21.6%, Europe at 20.6%, and North America at 19.6% – a notably more even spread than in recent quarters, pointing to a continued broadening of the market’s growth. CALA contributes 9.3% and Africa 1%. Within MENA, the UAE accounts for 59% of the region’s Q4 additions, with Egypt at 15% and Morocco and Saudi Arabia at 7% each. North America’s growth is almost entirely US-driven at 95%. APAC’s is more distributed with Thailand at 19%, followed by Japan, India, and Indonesia each at 14%. Europe once again leans on Georgia at 30%, with Portugal at 15% and Spain and the UK at 10% each.

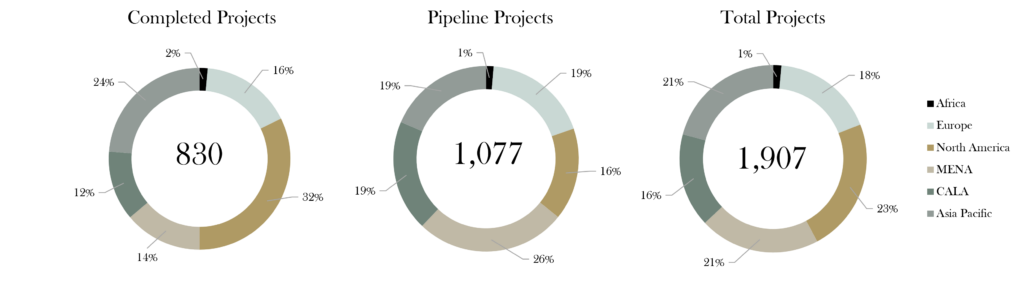

Looking at the full global base of 1,907 projects, North America holds the largest share at 23%, with APAC and MENA at 21% each, Europe at 17%, CALA at 16%, and Africa at 1%. The pipeline alone tells a different story: MENA leads at 26%, with CALA at 19%, Europe and APAC at 18% each, and North America at 16%. This gives a clear signal of where the market’s pipeline is heading.

This Quarter’s Market Spotlight – CALA; This quarter’s spotlight turns to Central America, Latin America and the Caribbean. With Sao Paulo taking the third place position, displacing New York (Completed and Pipeline), a pipeline share that now matches Europe and APAC, and growing diversification beyond Mexico, CALA represents one of the sector’s most interesting regions with further expansion potential.